The Veto Points

Why industrial projects fail after approval - and how to map the hidden constraints before they trigger

The Ledger has a new structure: field reports from inside complex systems - the moments operators discover where power actually sits - plus a living index of constraints that updates each quarter. Here’s Issue #8.

THE OPENING ENTRY

Insurance isn’t an input. It’s a permission system.

So is grid interconnection. So are credit ratings. So is water allocation.

Whoever runs the permissions decides what gets built in the 2030s - not who has the capital.

Grid capacity gets pre-committed by whoever asks for 200 MW first. Sovereign borrowing costs move 80 basis points because three analysts update a model. A fab expansion dies in a water district meeting the chip executives never attended.

Leaders make one repeatable mistake: assuming decisions happen where they’re announced - in boardrooms, at policy summits, in shareholder presentations. Spend time in underwriting, interconnection studies, and trade finance, and you see something different.

Decisions happen at the veto points. Usually late. Usually offstage. And most organisations don’t know where theirs are.

This week’s Ledger: five field reports from the control room, one pattern that connects them, and the five questions I would ask before greenlighting anything that matters.

FIELD REPORTS

Western Germany - The Late Veto

Two years of negotiation. €340M capex approved. Three German banks committed. Energy contracted. Works council aligned. Local government ready.

An analyst in a Swiss reinsurance office runs the facility’s coordinates through a climate-risk model.

Three days later, the insurance premium wipes the IRR. Nothing on the ground changed. The model did.

The plant was shelved. Not because of technology. Not because demand disappeared. Not because the board lost confidence.

Because the veto arrived after the sunk cost - when reversal was ruinous.

One of the senior members on the team told me later: “We spent two years negotiating everything we thought mattered. But because it wasn’t underwritten it didn’t happen.”

Southeast Asia - The Invisible Constraint

Perfect setup. Margins worked. Quality locked. Lead times hit the model. Contract ready to sign.

Then we discovered a major carrier had pre-sold their regional container capacity for eighteen months - to a competitor we didn’t know was moving.

The factory existed. The ships existed. The containers existed.

We just didn’t exist in that queue.

The constraint wasn’t on our spreadsheet. We’d modelled labour, energy, regulatory risk, IP protection, quality control. Six months of negotiation. Never thought to model the container market as a veto point.

By the time we discovered it, we’d committed to timelines, to downstream customers, to production planning.

The contract died. Not because of anything we negotiated. Because we treated capacity as an input when it was actually a constraint - and someone else had moved first.

Desert Southwest, United States - The Wrong Ministry

Everyone’s tracking semiconductor capex, construction timelines, workforce development. The models assume the constraint is capital, technology, or talent.

It’s water.

Advanced fabs need 7-20 million litres per day. Each. The water exists. The allocation structure doesn’t - because it was designed for agriculture in the 1950s, not advanced manufacturing in 2025.

The federal department is allocating strategic funding based on supply chain resilience and technical capacity. Those are the stated variables.

The binding variable is being decided in water district board meetings that chip executives don’t attend.

By the time the semiconductor industry realises water rights are the constraint, the allocations will already be committed to municipal growth, agriculture, and whoever asked first.

August 2024 - The Model That Constructs Reality

A major ratings agency downgraded a sovereign on climate exposure. Not fiscal mismanagement. Not political instability. Physical climate risk.

Borrowing costs jumped roughly 80 basis points overnight. For a country with $200B in outstanding debt, that’s $1.6B per year in additional interest expense - because a methodology changed.

Downstream, trade finance tightened for manufacturers who’d never missed a payment. Working capital costs spiked. Margins compressed.

The downgrade became self-validating.

The government could publish its own models, its own fiscal projections, its own climate adaptation plan. Didn’t matter. The market priced to the rating, not to the government’s view of itself.

I saw this in supplier finance constantly. Strong cash flow, solid operations, healthy order book - but if the credit rating dropped because of macro factors outside their control, their cost of working capital would spike. Which would squeeze operations. Which would validate the downgrade in retrospect.

Ratings agencies don’t predict risk. They construct it - by changing the cost of capital for everyone downstream.

Western United States, 2023-24 - The Silent Redraw

Major insurers withdrew completely from high-risk states. Not selective. No new homeowner policies in regions representing trillions in property value.

You can’t get a mortgage without homeowner’s insurance. You can’t get homeowner’s insurance in high-risk zones any more.

De-facto exclusion zones emerged via catastrophe models few outsiders ever see.

When we were evaluating warehouse sites, we’d find the optimal location - ports, labour, road access, distribution logic. The financial model worked.

Then the insurance renewal quote would come back and total cost of ownership would jump 40%.

The site hadn’t changed. The risk hadn’t materially changed. But someone’s forward loss curve had changed, and that was enough.

Six months negotiating property, labour agreements, local incentives. Three days for insurance. But those three days held the veto.

The asymmetry: insurers have privileged information about risk distribution that no one else can access until they choose to reprice. By the time you discover insurance has made your region uneconomic, you’ve already committed capital, time, political capital, and reputation.

The veto doesn’t announce itself. It just quietly refuses to underwrite. And the entire chain of decisions collapses backward.

WHAT THE LEDGER REVEALS

Five different situations. Five different industries. Same underlying structure.

In each case, the decisive actor controlled:

A non-substitutable input (coverage, queue position, water rights, rating, container capacity)

At a late-stage veto point (after sunk costs, after momentum)

Enabled by privileged information (risk models, allocation data, demand forecasts)

With lock-in dynamics (once committed, reversal is prohibitively expensive)

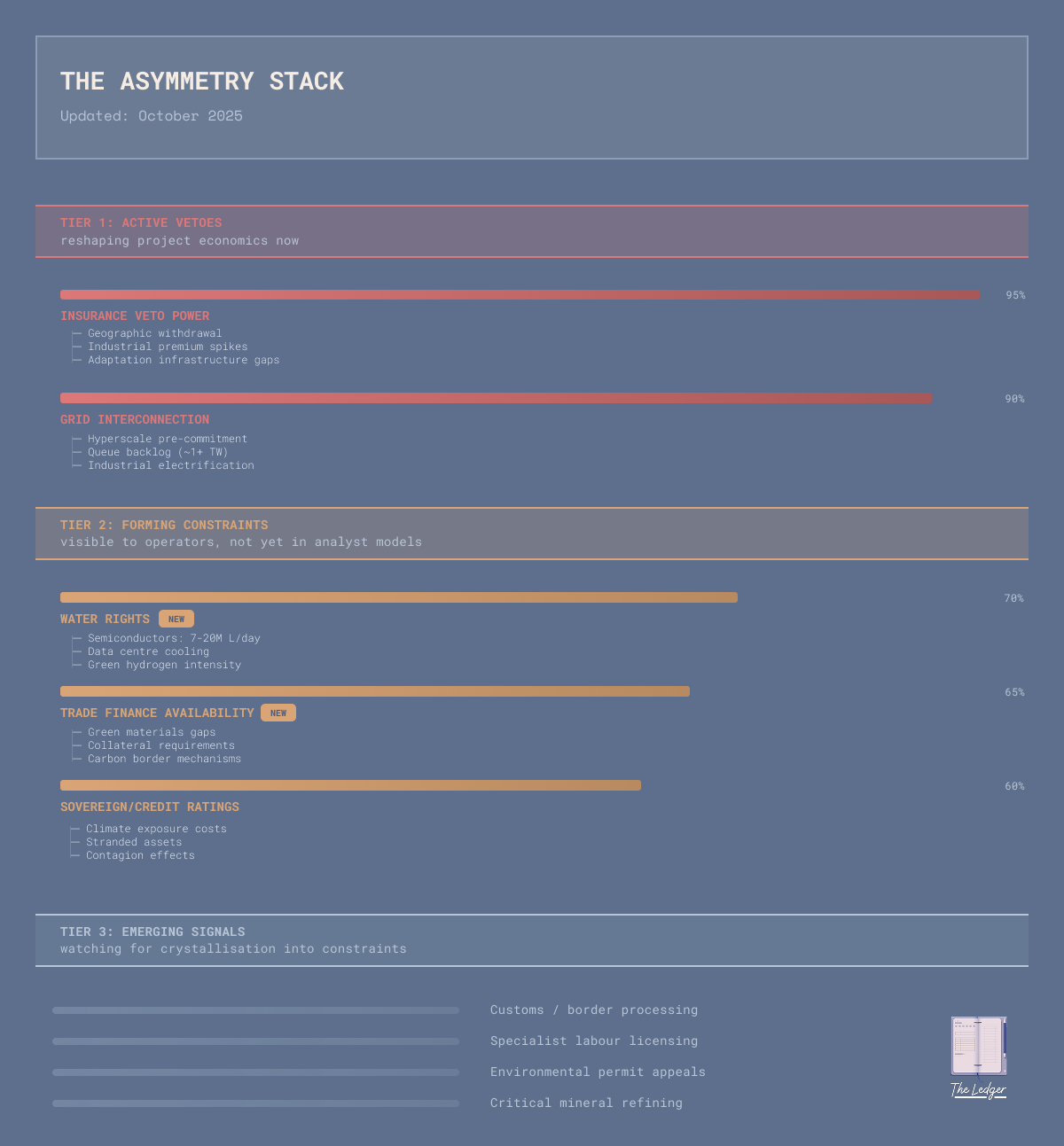

This is The Asymmetry Stack - the layered structure of hidden constraints that actually determines what gets built, where, and how fast.

Most strategic planning assumes constraints are visible, negotiable, and priced. But the constraints that kill projects are usually invisible until they trigger, non-negotiable when they do, and discovered after you’ve locked in.

The organisations that win in the 2030s won’t be the ones with the most capital. They’ll be the ones who map the veto points before they activate.

THE OPERATOR’S PLAYBOOK

Five questions I would now always ask before greenlighting any major decision. Not after the analysis - before we start building the model.

These aren’t consultant questions. They’re control-room questions. They assume power sits somewhere you haven’t looked yet.

1. Map the veto sequence, not the org chart

Who can say “no” after you’ve already committed capital and reputation?

Early approvals are easy - everyone’s optimistic, the vision is compelling. Late-stage vetoes destroy value because by the time they trigger, you’ve sunk everything.

The power sits at the late vetoes, not the early approvals.

List every “no” that can come after you’ve committed. Then build relationships at those veto points first - underwriters, interconnection study leads, water districts, export credit desks, permit appeals bodies.

Don’t treat them as procurement steps. Treat them as the people who actually decide if you’re building anything.

2. Name the one non-substitutable input

What single input, if it became unavailable or prohibitively expensive, makes this project impossible - not harder, impossible?

Most teams model the inputs they can price: capital, labour, materials, energy. But the binding constraint is almost never in your negotiated line items.

It’s in what you assumed would be there: coverage class, queue position, water allocation, container capacity, specialist labour, trade finance.

The asymmetry hides in what you treat as background.

If your answer is “nothing would kill it - we have backup plans,” you haven’t found the real constraint yet. Keep looking.

3. Model the model

Who holds better data than you do about a variable that matters?

Asymmetries thrive in information gaps. If one actor has vastly superior information about something critical, they control the outcome - even if they don’t own the assets.

Insurers have better catastrophe models than anyone buying coverage

Ratings agencies have better default models than most borrowers

Hyperscalers have better demand forecasts than utilities planning capacity

Logistics providers have better utilisation data than shippers

Information asymmetry is power asymmetry.

Figure out who’s modelling your constraint better than you are. Then either build that capability internally, or build a relationship with whoever holds it. Ask for assumptions, not conclusions - event sets, exceedance curves, load shapes, attrition factors.

Don’t wait for the market to reveal the constraint. By then you’ve already lost optionality.

4. Find the lock-in moment

Where do your options collapse from many to one? When does reversibility disappear and switching costs become prohibitive?

Asymmetries crystallise at lock-in points:

Technology choices that determine architecture for years

Supplier integrations that create data dependencies

Financing structures that limit operational flexibility

Regulatory pathways that create path dependence

Infrastructure commitments that fix location

The asymmetry isn’t in having choices. It’s in understanding what happens when choices collapse.

Map your lock-in sequence. Then either delay lock-in until you’ve cleared the veto points, or make sure you’re locking in to a structure that won’t become your constraint in 18 months.

5. Pre-wire the backstop

If the veto hits - if insurance reprices, if the queue study comes back delayed, if the water allocation can’t be secured - what’s your alternative?

Don’t build contingency slides. Build pre-negotiated alternatives:

Parametric coverage for gaps in traditional insurance

Capacity swaps or secondary interconnection points

Alternative water sources or usage-reduction commitments

Secondary supplier relationships with integration already tested

Trade finance alternatives lined up before primary falls through

Backstops negotiated in advance are strategic options. Backstops negotiated under pressure are expensive failures.

THE STACK

A living index of asymmetries I’m tracking - where power is shifting in ways most models aren’t capturing yet. This uses the same systematic approach I apply when evaluating industrial projects: tracking signals, validating evidence across multiple sources, and assigning confidence levels based on operator observations.

[NEW] marks this issue’s additions.

How items move between tiers: Signals graduate from Tier 3 → 2 when multiple operators in different regions report the same constraint independently. They move from Tier 2 → 1 when project economics are actively breaking - when operators are killing projects or fundamentally restructuring deals because of the constraint. Items retire only when mitigations become standard practice (e.g., when parametric insurance for a specific risk becomes widely available and affordable).

FIELD NOTES

Three conversations this week flagged the same asymmetry forming in different domains - transmission interconnection delays spreading beyond renewables into industrial projects. That’s a pattern forming, not isolated incidents.

Grid-scale solar developer, southern United States:

“Power purchase agreement signed 18 months ago. Interconnection study just came back - add 30 months minimum before energise. Economics modelled assuming twelve. Now renegotiating everything. The queue is the market.”

Property fund operator, coastal region:

“Commercial property insurance premiums up 40-60% at every renewal. No claims filed. Model updates only. Cap rates that worked in 2023 don’t work in 2025. We’re selling not because fundamentals changed - because someone updated a hurricane model.”

Green hydrogen project, southwestern United States:

“Electrolyser economics work. Power supply works. Offtake committed. We need roughly 400,000 cubic metres annually. Water district can’t commit without triggering regional allocation review: 3-5 years. The constraint isn’t technology or capital. It’s 1950s water law.”

If you’re seeing interconnection delays spreading beyond renewables into manufacturing, data centres, or other industrial operations - I want to understand where this constraint is binding and whether it should move from Tier 2 to Tier 1. Reply with what you’re seeing.

What I’m tracking:

Several recent conversations highlighted customs and border processing capacity becoming a bottleneck in nearshoring strategies. The physical infrastructure exists (ports, lorries, warehouses), but processing capacity at borders is adding 2-3 weeks to supply chains modelled for 48-hour clearance.

If you’re seeing this constraint activate in your operations - especially where multiple tariff regimes intersect - send me the details. I want to understand where it’s binding first and how rapidly it’s spreading.

THE LEDGER ENTRY

Systems don’t fail where you’re watching. They fail at the veto points you didn’t know existed.

Send me your field reports:

If you’re seeing an asymmetry form in your domain - a veto point crystallising, an assumption breaking, a constraint that’s not in anyone’s model yet - I want to hear about it.

The best intelligence doesn’t come from analysts watching markets. It comes from operators watching the system break in real-time.

You can reply or reach me at hello@tldgr.com

Here’s to what’s possible

Dom

The Ledger is a weekly field report on where power actually sits in complex systems.

Subscribe at tldgr.com · Read the archive